Publication

La Cour suprême du Canada tranche : les cadres ne pourront se syndiquer au Québec

Le 19 avril dernier, la Cour suprême du Canada a rendu une décision fort attendue en matière de syndicalisation des cadres.

Australie | Publication | décembre 2019

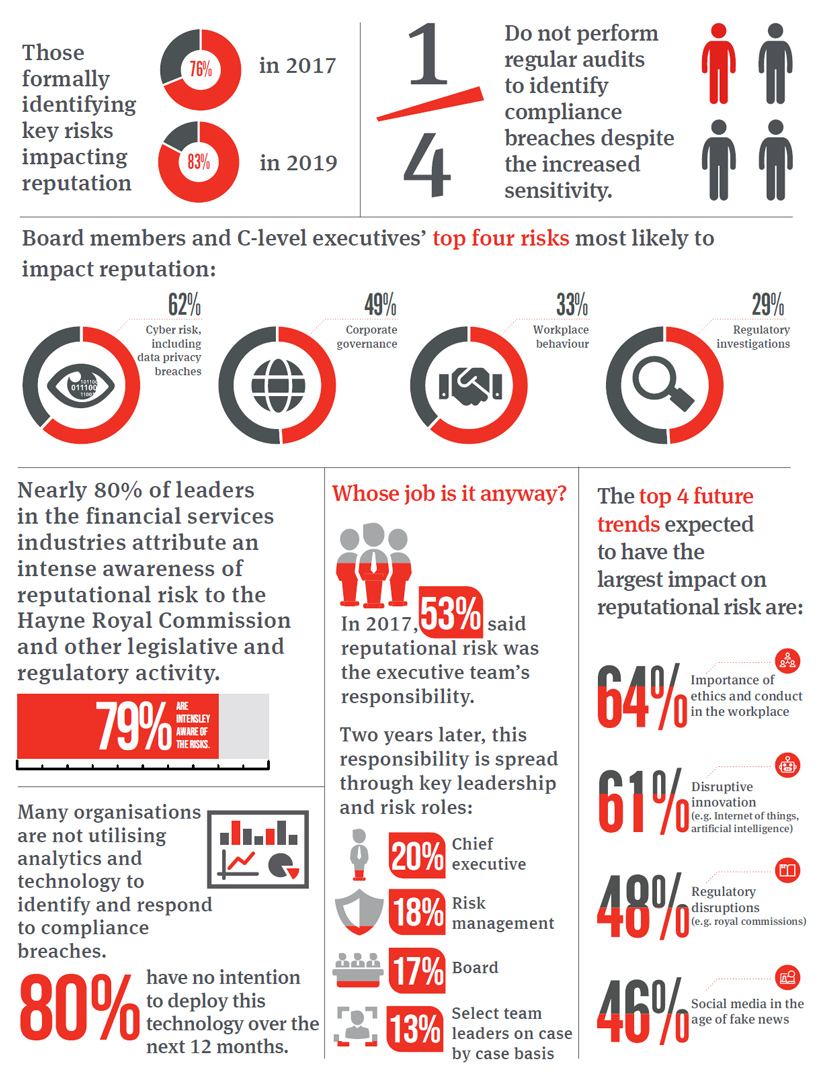

When it comes to questions of reputation in the workplace, the shadow of the Hayne Royal Commission hangs heavy over major Australian organisations.

In the year of Hayne’s landmark report on the conduct of Australian financial institutions, measuring, assessing and improving workplace culture has taken on new urgency and heightened feelings of exposure to reputational risk issues.

Norton Rose Fulbright surveyed 132 leaders across business and government between August and September 2019 to further its understanding of what reputational risk means to today’s organisations. The results of this research, taken together with the views gathered in our inaugural Reputational Risk Australia report in 2017, are detailed in this report.

The results clearly show a growing intensity of concern about workplace reputational issues. Major organisations are becoming both more sensitive to reputational risk and more willing to identify its key drivers.

To find out more about what reputational risk means to Australian organisations and benchmark your business against your peers, read our full report.

For more information, contact one of our employment and labour and risk advisory experts below.

Publication

Le 19 avril dernier, la Cour suprême du Canada a rendu une décision fort attendue en matière de syndicalisation des cadres.

Publication

Le budget 2024 propose d’élargir la portée de certains pouvoirs permettant à l’ARC de demander des renseignements aux contribuables tout en prévoyant de nouvelles conséquences pour les contribuables contrevenants.

Publication

L'impôt minimum de remplacement (IMR) est un impôt sur le revenu additionnel prévu dans la Loi de l’impôt sur le revenu (Canada) (la « Loi ») auquel sont assujettis les particuliers et certaines fiducies qui pourraient autrement avoir recours à certaines déductions et exemptions et à certains crédits pour réduire leur impôt sur le revenu fédéral canadien régulier.

Abonnez-vous et restez à l’affût des nouvelles juridiques, informations et événements les plus récents...

© Norton Rose Fulbright LLP 2023